November 4, 2022

A Look at Bear Market Rallies

Equities saw a strong rebound last month, with the S&P 500 gaining 8% and the Dow posting its biggest October ever¹. After this move, many investors have been left wondering if the bear market is over and if equities are kicking off a new bull market. In this week’s commentary, we explore historical bear market rallies and outline why we believe the move in October was likely not the start of a new bull market.

Bear Market Rallies are Common

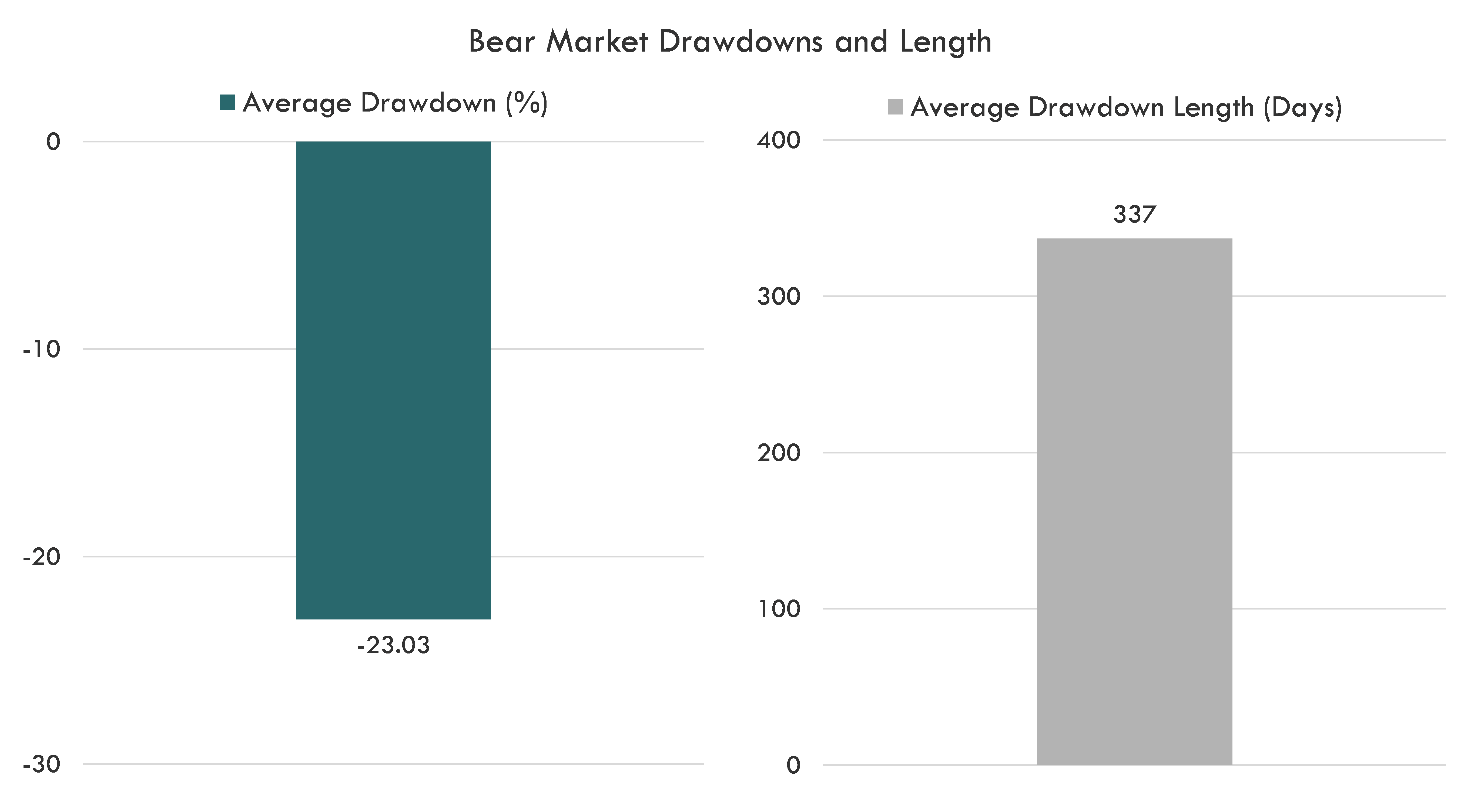

Bear markets tend to be drawn-out events and drawdowns are never point-to-point. Since 1928, the average bear market has gone on for 337 days, with an average drawdown of 23%.².

Source: Bloomberg LP, Innovator Research & Investment Strategy, S&P 500 Index. Data from 8/31/1929 to 3/31/2020.

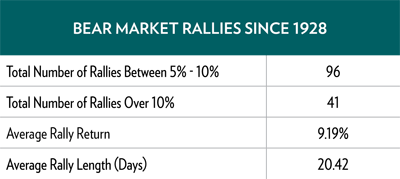

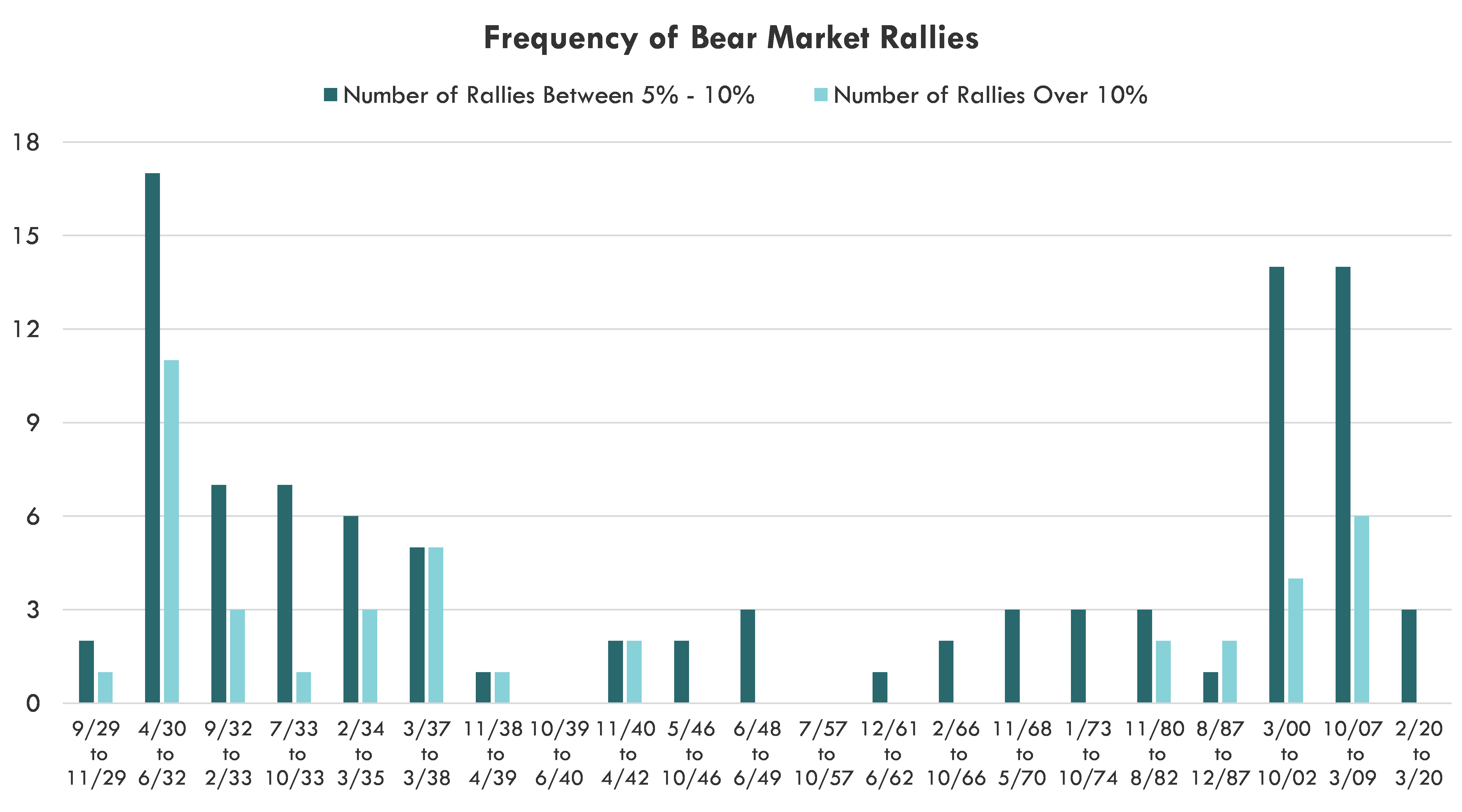

Intra period rallies, however, are very common. As shown in the table below, rallies of 5% or more have taken place in all but two of the twenty-one bear markets since 1928 and rallies of 10% or more have taken place in all but nine. The average rally has been just over 9%, lasting an average of 20 days.

We also see that these head fakes can often occur multiple times before the market finally finds a bottom. Rallies of 5%+ have occurred an average of 7 times per bear market, prior to the market bottom.

Source: Bloomberg LP, Innovator Research & Investment Strategy, S&P 500 Index. Data from 8/31/1929 to 3/31/2020.

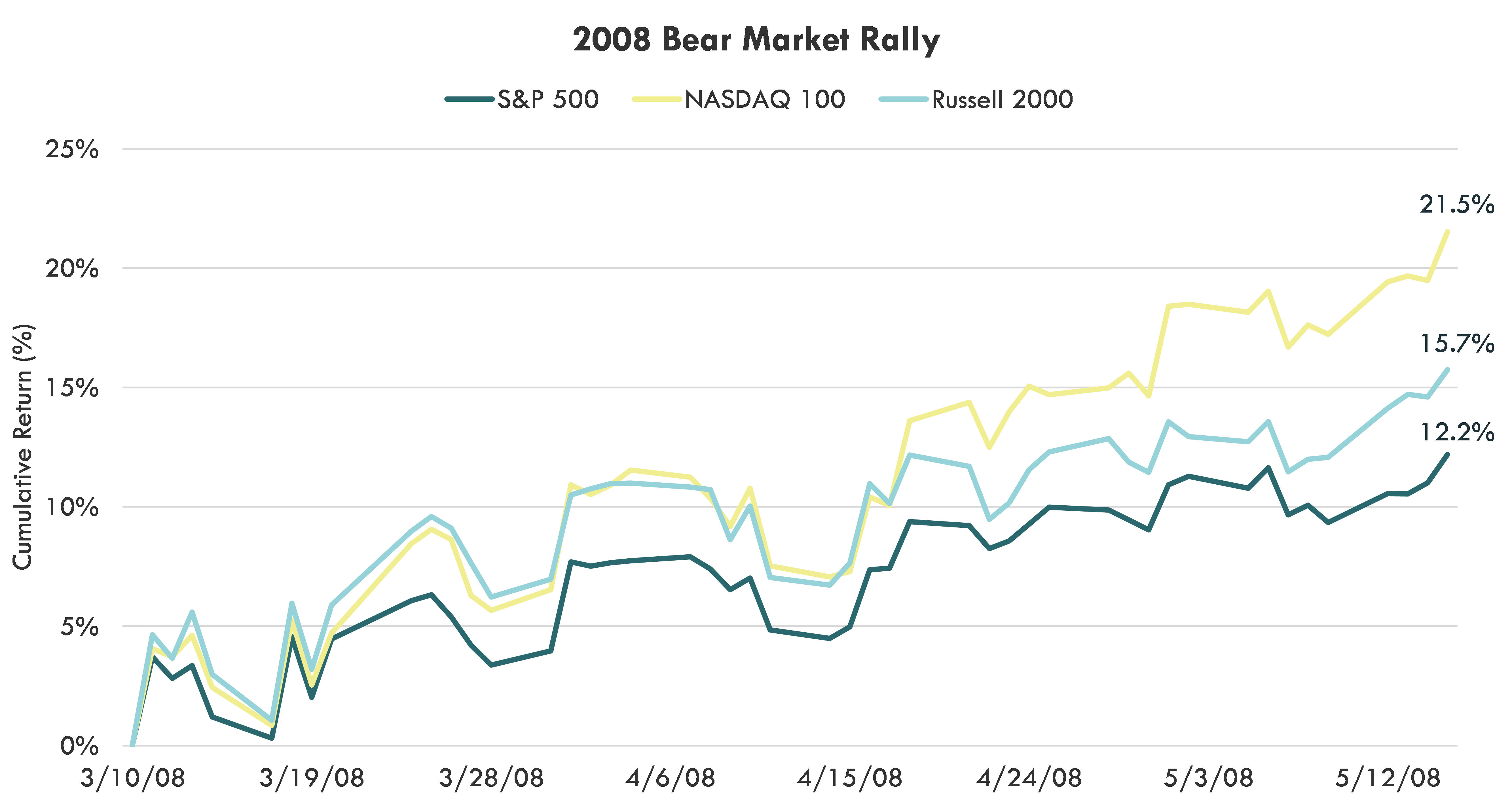

Source: Bloomberg LP, S&P 500 Index, Nasdaq 100 Index, Russell 2000 Index. Data from 8/31/1929 to 3/31/2020.

Bear Market Rallies can be Substantial

Not only are bear market rallies common, but some can also be substantial. The spring of 2008 provides a good example of this; the Fed continued to cut interest rates in the spring of 2008 and the S&P 500 rallied over 12%, the Nasdaq rallied over 20%, and the Russell 2000 Index 15%, only to see their values fall about 50% over the next ten months.

Source: Bloomberg LP from Innovator Research & Investment Strategy, S&P 500 Index. Data from 3/10/2008 to 5/12/2008.

Past performance is not indicative of future results. It is not possible to invest in an index.

October was Likely a Head Fake

There are several reasons why we believe the current market rally is in fact a bear market rally, and not the start of a new bull market.

1. We do not believe the equity market is reflecting the hit to growth that will be required to see a meaningful move down in inflation. While the path to a soft landing is indeed open, a recessionary fix to the inflation dilemma remains the higher probability event in our view and consistent with what has been required historically. A soft landing with core inflation north of 5% would be a first and should be treated as such. (See: What to Watch- Equity Valuations & Recession)

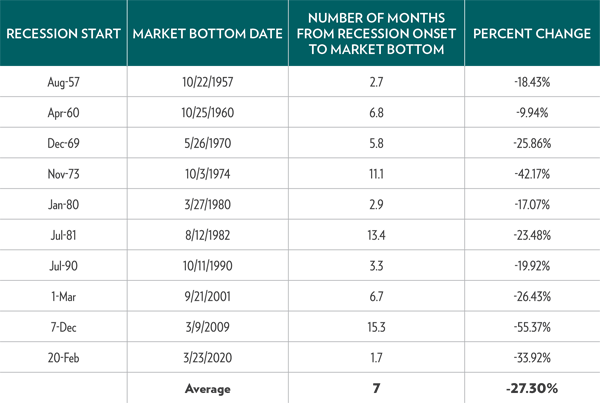

2. If we do see a recession, we do not expect the market to find a bottom beforehand. Historically, markets have bottomed an average of 7 months post-recession on-set and have never done so pre-onset³. At this point, with Fed tightening still going strong, equity valuations still elevated, and a potential recession ahead, those in search of a new bull market will likely need to be patient.

Source: Bloomberg LP, Innovator Research & Investment Strategy, S&P 500 Index, National Bureau of Economic Research. Data from 12/31/1956 to 12/31/2021.

The Bottom Line

Bear market rallies may present short term opportunities, but can easily be confused with the start of a new bull market. This time, we believe markets could take time to bottom as Fed action begins to filter into the economy and corporate earnings. As such, investors may find value in strategies that seek to accelerate positive short term market moves, as well as strategies that seek to hedge or buffer equity drawdown risk.

1. Source; Bloomberg LP as of 11/2/2022

2. Source: Bloomberg LP as of 11/2/2022

3. Data observed from 1957-2022, Recessions prior to 1957 were not taken into consideration

A bear market rally is a brief period of optimism that drives prices up temporarily before bearish sentiment takes hold once again and capitulation (panic selling) resumes, pushing prices even lower than before.

A bull market is the condition of a financial market in which prices are rising or are expected to rise.

The Nasdaq 100 Index is a basket of the 100 largest, most actively traded U.S companies listed on the Nasdaq stock exchange. The Russell 2000 Index is a stock market index that measures the performance of the 2,000 smaller companies included in the Russell 3000 Index.

The funds only seek to provide their investment objective, which is not guaranteed, over the course of an entire outcome period. Investors who purchase shares after or sell shares before the end of an outcome period will experience very different outcomes than the funds seek to provide.

The Funds have characteristics unlike many other traditional investment products and may not be suitable for all investors. For more information regarding whether an investment in the Fund is right for you, please see Investor Suitability in the prospectus.

The Funds are designed to provide point-to-point exposure to the price return of a reference asset via a basket of Flex Options. As a result,

the ETFs are not expected to move directly in line with the reference asset during the interim period. Additionally, FLEX Options may be less

liquid than standard options. In a less liquid market for the FLEX Options, the Fund may have difficulty closing out certain FLEX Options

positions at desired times and prices.

Fund shareholders are subject to an upside return cap the Cap that represents the maximum percentage return an investor can achieve from an investment in the funds for the Outcome Period, before fees and expenses. If the Outcome Period has begun and the Fund has increased in value to a level near to the Cap, an investor purchasing at that price has little or no ability to achieve gains but remains vulnerable to downside risks. Additionally, the Cap may rise or fall from one Outcome Period to the next. The Cap, and the Funds position relative to it, should be considered before investing in the Fund. The Funds website, www.innovatoretfs.com, provides important Fund information as well information relating to the potential outcomes of an investment in a Fund on a daily basis.

The Funds only seek to provide shareholders that hold shares for the entire Outcome Period with their respective buffer level against

reference asset losses during the Outcome Period. You will bear all reference asset losses exceeding the buffer. Depending upon market

conditions at the time of purchase, a shareholder that purchases shares after the Outcome Period has begun may also lose their entire

investment. For instance, if the Outcome Period has begun and the Fund has decreased in value beyond the predetermined buffer, an

investor purchasing shares at that price may not benefit from the buffer. Similarly, if the Outcome Period has begun and the Fund has

increased in value, an investor purchasing shares at that price may not benefit from the buffer until the Funds value has decreased to its value at the commencement of the Outcome Period.