August 31, 2022

MWhat to Watch - A Long Road Ahead

Fed Chair Powell spooked markets last Friday warning there is going to be ‘some pain’ ahead for the economy and the American people. Powell’s comments reinforced our view that a Fed pivot is not coming anytime soon, despite the market’s expectations. While we expect the Fed to hike rates another 0.75% at the September meeting, we are keeping a close eye on three economic releases this week: ISM Manufacturing PMI, Non-Farm Payrolls, and Unemployment. Each will provide clues as to how much work the Fed may have left.

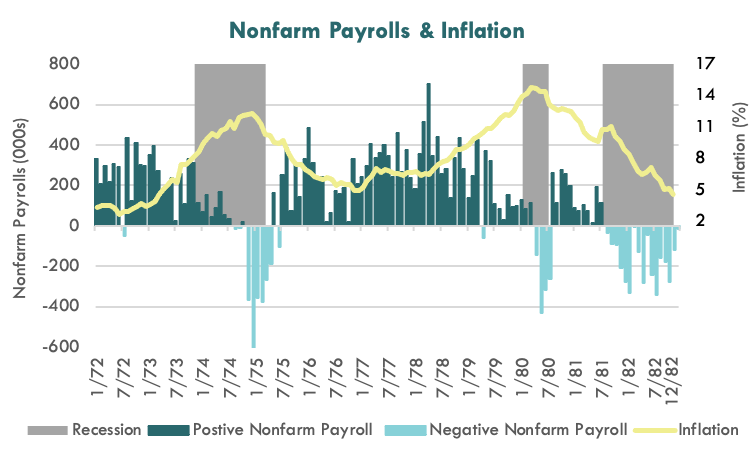

Nonfarm Payrolls

The labor market has been extremely resilient up to this point. Nonfarm payrolls posted a strong gain in August of 528k, well above average. While these gains may support the view that the economy is not yet in a recession it also highlights how much work still needs to be done, as inflation is unlikely coming down meaningfully, without a hit to the labor market.

We believe a perfect example of this is January 1972 to December of 1982. Even after multiple Fed hikes, Nonfarm Payrolls remained resilient, and actually did not turn negative until after the onset of each of the three recessions. As shown in the chart below, inflation really did not move lower until payroll growth turned negative. Should this week’s report continue to highlight the resilience of the labor market it will also likely highlight how long the rate hike cycle may have to go.

Source: Bloomberg LP, US Employees on Nonfarm Payrolls Total MoM Net Change SA, US CPI Urban Consumers YoY NSA, 1/31/1972 – 12/31/1982

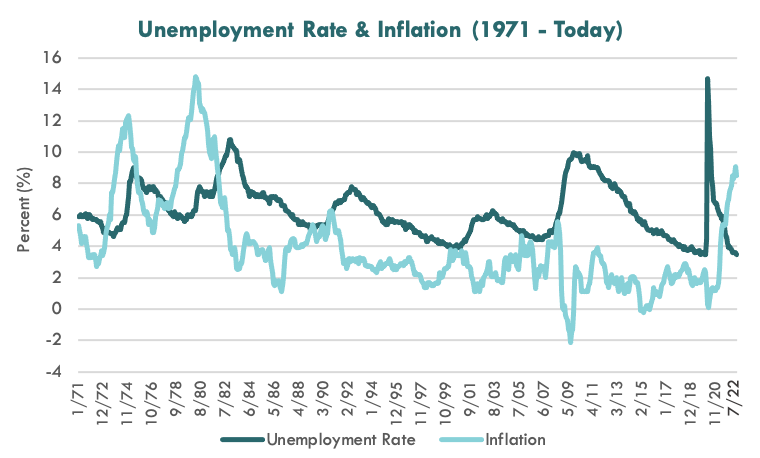

Unemployment Rate

Going hand in hand with Nonfarm Payrolls, the Unemployment Rate will be also be posted on Friday. August’s reading of 3.50% showed no signs of recent Fed action cooling demand for labor. Historically, since 1971, on average, unemployment has peaked approximately 19 months after peak inflation. In this context, the low rate of unemployment today is not surprising.

Source: Bloomberg LP, U-3 US Unemployment Rate Total in Labor Force Seasonally Adjusted, US CPI Urban Consumers YoY NSA, 1/31/1971 – 7/31/2022

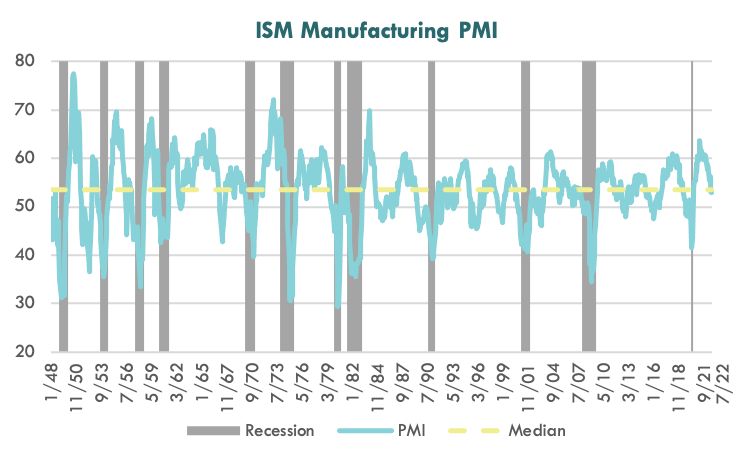

ISM Manufacturing PMI

While manufacturing data has softened recently (down 10% from the highs), last month’s reading of 52.8, still indicates the economy is expanding. It is also comfortably above the median recessionary reading of 43.5.

Source: Bloomberg LP, ISM Manufacturing PMI SA, 1/31/1948 – 7/31/2022

Manufacturing PMIs have a solid track record of identifying shifts in the business cycle. As such, we expect PMIs to continue to decrease as the Fed works to slow the economy. Any upside surprise could be viewed as a negative for the equity market.

The Bottom line

With the economy showing resilience to Fed tightening thus far, we expect another 0.75% hike at the September meeting. We believe the economy and more importantly the labor market needs to weaken further for inflation to come back down closer to the 2% target. Any “good news” this week will likely reinforce the long road that may be ahead.

The ISM Manufacturing PMI is a monthly indicator of economic activity based on a survey.