September 9, 2022

What to Watch - Under the Hood of Inflation

An encouraging CPI reading in July has many investors hopeful that inflation may have peaked. The recent drop was most heavily influenced by the decrease in energy, with gas prices falling 7.7%. Core personal consumption expenditures (PCE), the measure the Fed uses to determine policy, increased 0.3% MoM, but also came in better than feared. While we are optimistic that inflation has in fact peaked, when digging into the details, we believe it could be a long road ahead to get back to a reasonable level. Here are the three reasons why:

The Drop in Energy Prices has Been Somewhat Artificial

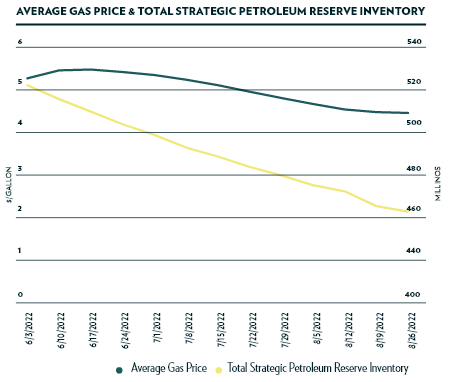

Energy prices declined 4.5% on a month over month basis in July, helping take down the overall CPI reading. The decrease was led by energy commodities and more specifically, a significant decrease in fuel oil. While the decrease was encouraging, it was somewhat artificially driven due to a release of strategic reserves along with a gas tax holiday in some states. According to the U.S. Department of Treasury, the release of petroleum reserves may have saved Americans~ 40 cents per gallon, accounting for ~37% of the decline in the price of gas.

|  |

| Source: U.S. Energy Information Administration, U.S. Ending Stocks of Crude Oil in SPR, 10/1/1977 – 6/30/2022 | Source: Bloomberg LP, DOE Strategic Petroleum Reserve (SPR) Total Inventory Data, US Average Gasoline Price, 6/3/2022 – 8/26/2022 |

In the near term, energy prices are likely to continue putting downward pressure on the headline figure, however, to see a sustained decrease, the underlying drivers of the energy crisis need to ease. The Russia Ukraine war, geopolitical sanctions, and supply chain disruptions have yet to fully resolve, and may remain a headwind to energy prices.

Shelter Costs are Sticky and Continue to Rise

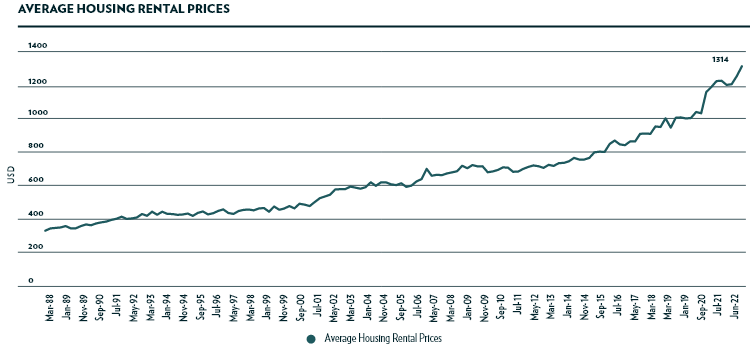

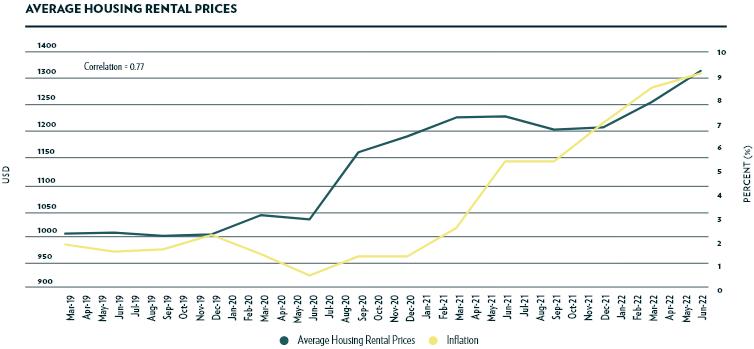

Shelter costs recorded their biggest gain since 1991, increasing 5.7% in July. Most notably, rent prices continued their trek higher, a journey that began all the way back in 2019.

Source: Bloomberg LP, Median Asking Rent In The United States, 3/31/1988 – 6/30/2022

Rent prices could pose a longer-term threat, as increases tend to be stickier and also do not decrease quickly. Since 1988, the biggest quarterly drop in rent prices came in at just -5.86% in 2007. Given the 32% weight of shelter in the CPI basket, getting rent prices down will be a big part of getting the headline figure back down. We believe this isn’t going to happen overnight and may be a longer process.

Source: Bloomberg LP, Median Asking Rent In The United States, US CPI Urban Consumers YoY NSA, 3/31/2019 – 6/30/2022

Food Costs Are at All Time Highs

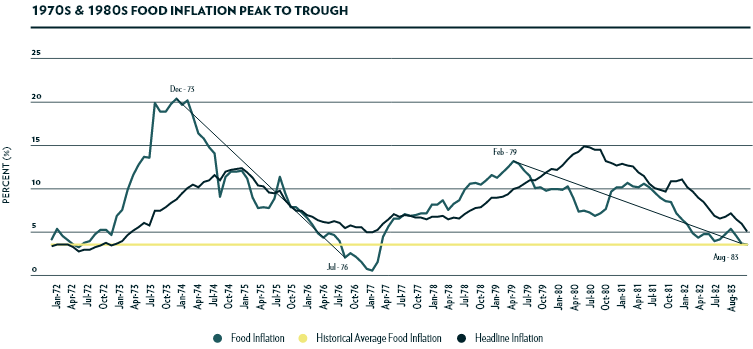

During the 1970s and 1980s, the last time inflation was this high, the price of food was consistently one of the leading drivers of inflation moving higher and moving lower. In the late 1970s, nearing the end of the high inflation environment, food inflation peaked at 13.1%. From that point on, it took an additional 44 months, or over 3.5 years, to retreat back to the historical average of 3.5%.

This time around, food costs still have yet to peak. In fact, in July, food costs recorded their biggest YoY jump since 1979 (+10.9% YoY). For headline inflation to come back to an acceptable level, the cost of food needs to come down, and just like shelter costs, this could take time.

Source: Bloomberg LP, US CPI Urban Consumers Food NSA, US CPI Urban Consumers YoY NSA, 1/31/1972 – 8/31/1982

The Bottom line

While the September reading may continue to support the narrative that inflation has peaked, we believe the level of inflation may stay elevated for some time.

The Consumer Price Index, or CPI, measures the overall change in consumer prices based on a representative basket of goods and services over time.

Personal Consumption Expenditures, or PCE, is an estimated total of personal consumption expenditures (PCEs) is compiled by the U.S. government monthly as one way to measure and track changes in the prices of consumer goods over time. PCEs are household expenditures.